Why Your Rent Is So High and Your Pay Is So Low

Tom Streithorst explains why stagnant wages and higher stock prices are two sides of the same coin.

By Tom StreithorstAugust 4, 2015

IN THE 1950s, the average New York City apartment rented for $60 a month — around $530 in today’s money. With the US median wage at $5,000 a year, New Yorkers spent 1/10 of their salaries on rent. After World War II, apartments were so cheap and available that Manhattanites would regularly move every September just to get the landlord to repaint their new home. In those days, an apartment was a place to live. Now it is as much an investment as shelter.

Imagine trying to find an apartment in Manhattan for $530 now. It is almost inconceivable. These days a depressing number of young New Yorkers spend over half their income on housing. Rent hikes have transformed a once-democratic city into a playground for the privileged. Hardly anyone can afford to move to New York on an entry-level wage. It sometimes seems that the only twentysomethings that come to New York today have parents who help pay the rent.

During the boom years after World War II, Americans’ real wages more than doubled. A 30-year-old earned twice as much by the time he or she hit 50. This broad-based prosperity transformed the nation. In 1939, 25 percent of Americans didn’t have running water, only 65 percent had indoor toilets, none had television. By 1970, almost all had cars and dishwashers. The luxuries of an earlier age had become necessities. Between 1945 and 1973, the United States and the world experienced the greatest economic growth in history, not replicated before or since. Economic historians call those postwar years the Golden Age.

This explosion of affluence did not extend to New York City landlords. Rent control kept rent increases lower than inflation. Apartment prices remained stagnant. In 1976, you could buy a classic four-bedroom Park Avenue apartment in a doorman building for $36,000. Owning a building back then didn’t make you rich. Instead it was a drain on capital. The fires that devastated huge swaths of New York in the 1970s were generally set by landlords who saw insurance fraud as the only way to profit from their properties. The average rent that decade was just $335. You could rent a two-bedroom apartment in Greenwich Village for $250 a month.

The 1970s have a bad reputation amongst pundits and policy makers, but for most working people they were pretty good. Inflation-adjusted wages went up more in the 1970s than they have any decade since. For rich people, however, the 1970s were terrible. The stock market tanked, the bond market was even worse, corporate profitability collapsed, and, with inflation higher than interest rates, putting money into the bank only confiscated wealth.

In both Britain and America, unions were strong, strikes were common, management no longer in control of the shop floor. The average union cameraman made more money than the average banker. Then, everything changed. In 1982, wages stopped going up, while asset prices (stocks, bonds, real estate) began their spectacular rise.

The Reagan/Thatcher revolution can best be understood as the counterattack of capital, enraged by labor’s depredations. Central banks here and in Britain engineered the most brutal recession since the 1930s by raising interest rates until the economy screamed. Unemployment and bankruptcies soared; businessmen, politicians, and unions pleaded for a rate cut, but Paul Volcker and Nigel Lawson were implacable in their conviction that pain was necessary in order to crush inflationary expectations. Economists have long recognized the relationship between unemployment and inflation. When workers fear for their jobs, they don’t ask for raises.

Reagan, Thatcher, Volcker, and Lawson succeeded beyond their wildest dreams. Inflation, which hit 13 percent in 1980, has only exceeded 5 percent once since 1983 and generally has been under 3 percent. Labor’s demand for cost of living increases sparked the 1970s inflationary spiral, and once wages stopped going up, so did inflation. Unfortunately, workers are still paying the price for its elimination. Today, median male real wages in America are lower than they were in 1973.

By reducing worker pay, Reagan and Thatcher made corporations more profitable. By ending inflation, they made owning bonds one of the great investments of our time. In 1982, the Dow Jones Industrial Average bottomed out at 776. Today it is over 18,000, a rise of more than 2,300 percent in 33 years. Interest rates have fallen from over 15 percent to barely above 0 percent. And house prices began their inexorable climb. By the 1980s, the average New York apartment rented for $1,700 a month (which is $3,700 in 2015 dollars).

Every economy has to answer two questions: how much to produce and how to distribute that production. Technological advances ensure that each year we can make more stuff with less labor and capital than the year before. This has not changed. What has changed is how we allocate the benefits of progress. Back in the day, workers got the money; today, owners of assets do. Stagnant wages and higher stock prices are two sides of the same coin.

During the Golden Age, productivity increases almost immediately translated into wage increases. As technology made workers more productive, their wages went up commensurately. Since 1982, technology and productivity have continued their inexorable rise, but wages have not reflected that growth. The benefits of productivity increases have gone instead to the richest segments of society, or more precisely to the owners of assets, to those who own stocks, bonds, or real estate.

A few years ago, at a rooftop corporate party in central London I was chatting with the fiftysomething guitarist hired to entertain us. Bitterly, he told me he used to be an advertising art director — that a decade or two ago, he flew around the world making high-end TV commercials. Now, he couldn’t get arrested. Despite his skills and experience, no advertising agency was even interested in hiring him freelance. “Thank God I bought a house 20 years ago when I could afford it,” he told me. “That is the only thing I can leave my kids.” Jobs aren’t for life anymore, but property is.

Once upon a time, we saved for our retirement by having lots of children, hoping some of them lived to adulthood and continued to love us. In our dotage, unable to work, we could lie in a dark corner of their shack and eat our portion of gruel while they tilled the fields.

By the mid-20th century, our retirement was no longer dependent on our children’s good will. In those days, both blue- and white-collar jobs were secure. If you gave your youth to the corporation, it would reward your loyalty and keep you on until you were 65 (even if you weren’t as productive as you used to be), at which point you would get a gold watch, a party, and a pension sufficient to pay your golf fees and allow you to take the occasional cruise.

Those days are long gone. Almost nobody has a job for life. More and more of us are freelance, hired on a job-by-job basis. If we get sick or injured or merely less cool than we used to be, our employer can forget he ever knew us and hire someone else. Risk has shifted from the corporation to the individual. And forget about working until you are 65. In a growing number of industries, once you are 50, you are well past your sell-by date. It seems the professional life cycle these days is get an unpaid internship in your early 20s, climb the ladder in your 30s, out the door at 45. Loyalty is a one-way street. Our employers see us as replaceable cogs. Once you reach a certain age, they hire someone younger who will happily grovel for less money.

Today, with job security and defined benefit pensions historical anomalies, the middle aged and middle class depend on rising house prices to fund their retirement. Of course, this is a gravy train that cannot last indefinitely. Forty years ago, in my now fashionable London neighborhood, houses sold for well under £30,000. Today, many are worth £2 million. Few young people can afford the down payment, and, anyway, for houses to continue to appreciate at this pace, these houses would have to be worth £128 million by 2055.

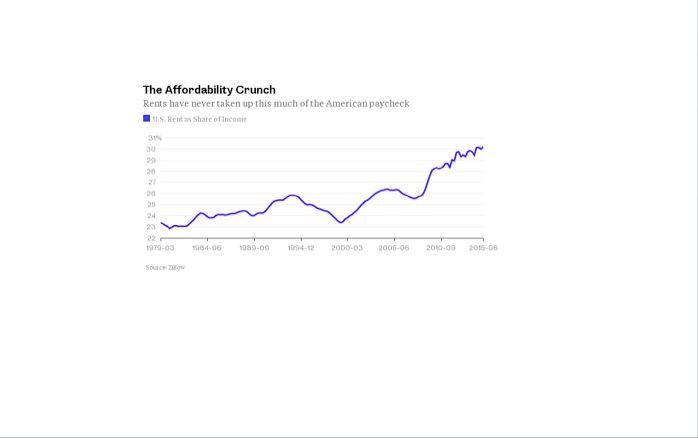

High real estate prices are good for the old and affluent. They are terrible for the poor and young. Today, the average Manhattan apartment rents for $3,800 a month, while median New York income is around $65,000 a year. If you are young and renting, your landlord eats his daily bread by the sweat of your brow. The flip side of affluent old people being able to retire is young people having to live with their parents.

If house prices fall, the middle aged and middle class will be in an uproar. For almost all of us, real estate is our principal, if not only, asset. If our house stops appreciating, our dreams of someday not having to work utterly evaporate. We vote and so politicians listen to our desires. Falling house prices would be a boon for renters and first-time buyers (and probably for society at large), but their political clout is less than that of middle-aged, middle-class property owners.

Perhaps even more critically, banks need house prices to rise, or at least not collapse. Traditionally, bank lending was to firms, providing small businesses or corporations investment and working capital. Today, most bank lending funds mortgages for families. What banks own, what offsets the liabilities they owe depositors, are mortgages. If house prices fall (as they did leading up to the financial crisis), so do the value of the mortgages underlying them. If they fall far enough, then banks become insolvent: the money they owe depositors exceeds the value of their assets. That, in essence, is what happened during the financial crisis. Had the government not backstopped the banks, you and I could quite easily have gone to the ATM, slipped in our card, and been told the money we thought was safe in our accounts was gone.

The fear of another financial crisis combined with the fear of angry middle-class, middle-aged voters gives politicians every reason to keep house prices from falling. During the Golden Age, strong unions and strictly regulated lending meant that wages went up faster than asset prices. No more. Today, the average home-owning Londoner earns more every year from rising house prices than he does from work. Easy credit, low interest rates, low down payments all stimulate ever-higher real estate values.

It isn’t as if government were impotent. Of course, demand for New York apartments has risen while demand for workers has fallen, but how we distribute society’s ever-growing wealth is at least in part a political decision. If they wanted to drive down rents, government could fund the construction of public housing, as they did during the Golden Age. More quality housing would increase its stock, and with supply rising to meet demand, prices would fall. This would be great for young renters, bad for middle-aged property owners, bad for banks. Thus it is not likely to happen. Property prices, at an all time high, are not likely to fall, and if they do, expect the government to put a floor under them.

During the Golden Age, affluence flowed toward labor. Today it flows toward asset owners. I think my retirement is safe. I’m not so sure about my children’s work prospects.

¤

Average Monthly Rent

ManhattanRent Inflation AdjustedAverage Hourly Wage Inflation AdjustedMedian Household Income Inflation AdjustedDow Jones Industrial Average Inflation Adjusted1940s$50$480$10$35,0002,0001950s$60$532$14$39,0004,0001960s$200$1,510$16$41,0006,0001970s$335$1,480$18$46,0003,0001980s$1,700$3,757$17$46,0003,5001990s$3,200$4,993$18$52,50010,0002000s$3,800$4,627$19$51,50014,000

¤

*Data Sources:

http://ny.curbed.com/archives/2013/11/21/what_would_50_in_1940_rent_a_new_yorker_today.php

http://www.usinflationcalculator.com/inflation/historical-inflation-rates/

http://inequality.org/income-inequality/

http://www.macrotrends.net/1319/dow-jones-100-year-historical-chart

¤

LARB Contributor

Tom Streithorst has been a union member, an entrepreneur, a war cameraman, a commercials director, a journalist. These days, he mostly does voiceovers and thinks about economic history. An American in London, he’s been writing for magazines on both sides of the pond since 2008. He is currently working on a book on how the incredible productive power of capitalism and technology have the potential to bring us all prosperity and happiness but so far, we keep screwing it up. He also writes a regular column about economics at pieria.co.uk.

LARB Staff Recommendations

Donald Trump, The Coen Brothers, and the Decline of the American Middle Class

Behind the angry talk of Trump supporters is the recognition that the world they were promised, the world of "Hail, Caesar!," is gone.

The Economics of Mad Max and Star Trek

Our scientific prowess and our destruction of the planet: which will be the first home to roost?

Did you know LARB is a reader-supported nonprofit?

LARB publishes daily without a paywall as part of our mission to make rigorous, incisive, and engaging writing on every aspect of literature, culture, and the arts freely accessible to the public. Help us continue this work with your tax-deductible donation today!